In the past decade, investors have increasingly sought out investment products that incorporate environmental, social and governance (ESG) criteria in their portfolio construction process. Some are seeking ways to align their investment portfolio with their values, while others see ESG criteria as important tools to assess a stock’s long-term performance potential. This growing demand has led to a variety of methodologies for implementing ESG strategies, some of which may create risks such as unfavorable industry concentrations and tracking error against market-cap weighted benchmarks.

In the past decade, investors have increasingly sought out investment products that incorporate environmental, social and governance (ESG) criteria in their portfolio construction process. Some are seeking ways to align their investment portfolio with their values, while others see ESG criteria as important tools to assess a stock’s long-term performance potential. This growing demand has led to a variety of methodologies for implementing ESG strategies, some of which may create risks such as unfavorable industry concentrations and tracking error against market-cap weighted benchmarks.

In this paper, we explain how an approach that integrates analysis of ESG key performance indicators (KPI) into traditional portfolio selection criteria may help overcome the limitations of other ESG strategies, while pursuing the potential for enhanced risk return profile. We then explain the methodology that the FlexShares STOXX US ESG Select Index Fund uses to generate a diversified core equity ESG portfolio.

THE CHALLENGES OF BUILDING A DIVERSIFIED ESG PORTFOLIO

Our research suggests that there is growing interest in ESG investing among investors who want to align their portfolios with their values, or who believe that ESG criteria can impact a company’s long-term business performance. In response, several methods for ESG investing have sprung up over time.

Some strategies exclude companies based on their business activities, such as oil drilling, tobacco products, or weapons production. Others seek to overweight so-called “best in class”1 ESG companies, those involved in activities with a social or environmental benefit as well as those demonstrating a commitment to add diversity to their corporate boards, and other positive changes.

Some of these approaches may come with important trade-offs, including limited diversification potential and the chance of weaker risk-adjusted performance. For example, excluding companies based on their activities alone could remove entire industries or sectors from investment portfolios, causing a potential increase in tracking error compared to market-weighted benchmarks. Similarly, selecting companies based solely upon their sustainability efforts could concentrate a portfolio in certain sectors.

Many investors have begun implementing ESG strategies that examine select ESG-related key performance indicators reported by public companies in their regulatory filings as a way to further assess a stock’s potential risk and returns. We believe that analysis of disclosed ESG data, combined with improved portfolio construction guidelines, may result in a more diversified, ESG tilted core equity investment portfolio. The resulting portfolio could help deliver the potential benefits of ESG investing while avoiding common pitfalls such as insufficient diversification.

APPLYING ESG KPIS IN THE PORTFOLIO SELECTION PROCESS

The FlexShares STOXX US ESG Select Index Fund is an ETF that seeks enhanced risk return characteristics relative to the broad large-cap US equity market from an ESG portfolio by tracking a custom index, the STOXX USA ESG Select KPIs Index.2 STOXX is a leading index provider in Europe, owned by the Deutsche Borse, which operates the largest stock exchange in Germany, and the SIX Swiss Exchange, the leading independent stock exchange in Europe.

The universe of stocks under consideration in the index starts with the U.S.-based companies listed in the STOXX Global 1800 Index.3 STOXX avoids investing in companies that operate in violation of the UN Global Compact, or have certain business involvement ties with tobacco, thermal coal, unconventional oil & gas, for profit prisons or weapons.

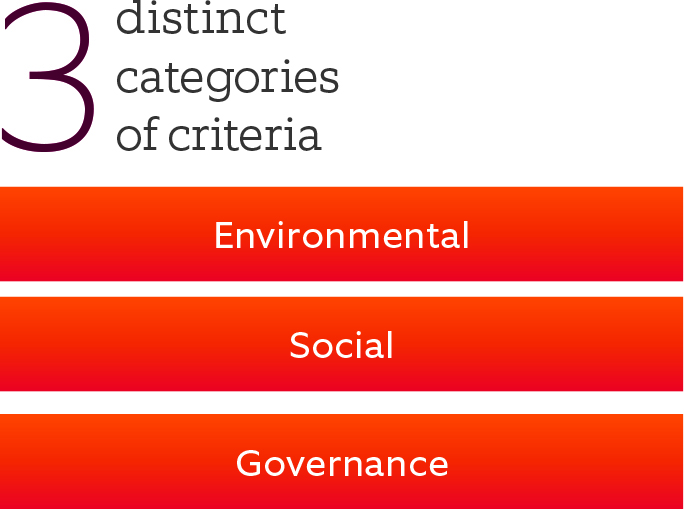

Next, the index employs bottom-up analysis of publicly available data to evaluate more than 150 ESG-related KPIs with broad representation among the three distinct categories of criteria—environmental, social and governance. STOXX pays particular attention to the KPIs its research has shown to have been most influential in determining risk and return. Based on this analysis, each stock receives an aggregate ESG score, and the bottom 50% of companies are excluded from the index.

Next, the index employs bottom-up analysis of publicly available data to evaluate more than 150 ESG-related KPIs with broad representation among the three distinct categories of criteria—environmental, social and governance. STOXX pays particular attention to the KPIs its research has shown to have been most influential in determining risk and return. Based on this analysis, each stock receives an aggregate ESG score, and the bottom 50% of companies are excluded from the index.

The custom index’s holdings from among the remaining 50% are tilted in favor of constituents with higher aggregate scores in an effort to optimize risk-adjusted return. Finally, constraints are applied in the portfolio construction process to maintain sector and style neutrality compared to the index. In addition, the final portfolio targets holdings of no more than 5% in any single company.

SEEKING IMPROVED DIVERSIFICATION AND ENHANCED RISK/RETURN PROFILE

We believe that measuring the impact of KPIs on a stock’s potential risk/return profile provides a holistic and diversified approach to ESG investing—one that identifies sustainable companies while potentially reducing portfolio risk and enhancing long-term investment performance.

Since the risks related to ESG criteria differ across industries, our research indicates it is prudent to evaluate the impact of KPIs on a sector-by-sector basis. By focusing on the ESG criteria that research has shown to be most material in specific sectors/industries, The STOXX USA ESG Select KPIs Index is designed to target companies that exhibit positive risk and return versus a market-cap weighted index. Composite ESG scoring may also help provide wider screening across all three categories of environmental, social and governance criteria.

We believe this bottom-up approach parallels best practices employed by a wide swath of portfolio managers when they evaluate, sort and select companies for other types of investments. Employing diversification controls for style and sector exposure may further enhance diversification, which we believe may help avoid the risks associated with ESG strategies such as exclusionary screening.

CONCLUSION

While ESG investments have grown in popularity, our belief is that the criteria used to evaluate ESG performance are not universally applicable across sectors. As a result, common selection methodologies may make ESG portfolios prone to sector concentrations and tracking error that unnecessarily limit opportunities.

The FlexShares STOXX US ESG Select Index Fund is designed to use a bottom-up approach to portfolio selection to help improve sector diversity and manage potential tracking error. By relying on a methodology that applies ESG scoring early in the selection process, the Fund integrates ESG principles with more traditional portfolio analysis tools to maintain a diversified core equity investment strategy while tilting toward ESG criteria. This methodology, along with sector and security constraints, may offer the potential for a broadly diversified ESG portfolio that can help align an investor’s portfolio with their values.

FOOTNOTES

1 Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market. This includes Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities and collateralized mortgage-backed securities.

2 The risk-return profile is an overview of how much the investment risk within the fund or strategy has the chance that the actual value of, or return from, an investment may be less than its expected value or return.

3 SIFMA, https://www.sifma.org/resources/research/fixed-income-chart/. At the end of each year, SIFMA calculates the total outstanding debt within the fixed income market from these categories Corporate Bonds, Mortgage-Backed Securities, Asset-Backed Securities, Federal Agency Securities, Treasury Securities & Municipal Securities beginning of 1996 to end of 2019. Each category is then assigned a percentage within the larger total of the combined categories.

4 Duration is how sensitive your investment or a portfolio is to a change in interest rates. You will often see it expressed as a number of years – the higher the number the more volatile will be the expected change. Historically, rising interest rates have often meant falling bond prices, while declining interest rates have meant rising bond prices.

5 Risk-adjusted yields defines an investment’s yield by measuring how much risk is involved in producing that yield, which is generally expressed as a number or rating.